Access to financial services is a critical component to solving some of the world’s most persistent problems, such as poverty and inequality. Yet, 1.4 billion people today do not have access to formal financial services. Financial inclusion is even lower for women and for people living in poverty.

OUR REACH

921,243

Borrowers

924,270

Savers

96%

clients are women

Microfinance is at the heart of BRAC’s holistic approach to development. We equip people who would otherwise be excluded from formal financial systems with the tools to invest in themselves, their families, and their communities.

Following decades of experience and insight in delivering financial services to populations living in poverty in Bangladesh, BRAC first expanded its microfinance operations internationally in 2002.

Our mission is to responsibly provide financial services to people who are excluded from formal banking sectors. We particularly focus on women living in poverty in rural and hard-to-reach areas, to help create self employment opportunities, build financial resilience, and harness women’s entrepreneurial spirit.

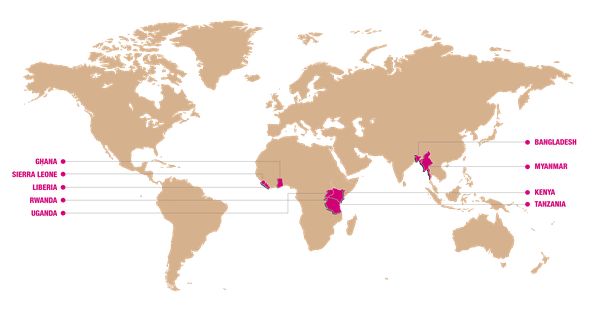

BRAC International Microfinance operates in seven countries outside of Bangladesh, with each company registered as a separate legal entity. This structure allows us to be locally responsive while aligned with our global mission of financial inclusion and poverty reduction.

WHERE WE WORK

OUR APPROACH

OUR APPROACH

Socially driven

To create a positive impact in the lives of our clients is our only bottom line. We deliver financial services in a way that is transparent, fair, and safe, adhering to the Universal Standards for Social Performance Management and the Client Protection Principles, placing clients’ well-being at the center of everything we do to achieve our mission.

Inclusive financial services

We offer inclusive, accessible, and convenient loan and savings products tailored to the needs of the local community, including women, smallholder farmers, small business owners, and youth. We complement these services with financial literacy training, enabling borrowers to make informed financial decisions.

Empowering women

When women have control of their finances, they are more likely to invest in family needs, such as health care, nutrition, and education for their children. We primarily focus on women, enabling them to become financially resilient and improve the quality of life of their families.

Digital innovation

The client value proposition is at the core of our digital transformation efforts, with a particular emphasis on reducing the gap in women’s digital financial inclusion. We are embracing financial technology by digitizing field operations and adopting alternative delivery channels to increase operational efficiency and offer greater convenience to our clients.

Holistic approach

Pairing microfinance with other social services can amplify the impact of our mission. We complement our microfinance services with many of our social development programs, such as youth empowerment, agriculture and food security, and livelihood programs.

OUR IMPACT

Microfinance, responsibly delivered, is a powerful tool to increase the inherent resilience and economic empowerment of people living in poverty.

By listening directly to the people we serve, we design financial services that create sustainable, measurable impact at scale.

We started to measure our social performance and client outcomes from 2019 using Lean Data℠ methodology on five focus areas of BRAC International Microfinance:

- Quality of life

- Financial resilience

- Women’s economic empowerment

- Self-employment and livelihood opportunities

- Household welfare

This annual survey complements our Social Performance Management and Client Protection initiatives, and helps us to set targets and refine strategies to reach more people living in poverty to achieve long-term impact.

The sixth impact survey was completed in 2025 using Lean Data℠ methodology in partnership with 60 Decibels. All respondents were women.

Highlights from 2023 Impact Survey

94%

of clients reported an improvement in their quality of life.

95%

of clients increased earnings.

94%

of clients managed their finances better.

90%

of clients saved more.

2021 Impact Brief

2022 Impact Brief

Capacity Statement

BRAC’s loans have helped and inspired me to expand my business when I could not find any other sources of capital. My business is growing day by day and I have more customers now.”

- Uwajeneza Brigitte, Rwanda

RESEARCH EVIDENCE

BRAC believes that sustainable, large-scale change must address and deliver both economic and social progress. Microfinance is an integral part of BRAC’s holistic approach to development, equipping people with the tools to invest in themselves, their families, and their communities.

BRAC International Microfinance (BI MF) has been measuring its social performance and desired client-level outcomes since 2019 using the Lean Data℠ methodology. Survey results from the past two years show that client-centric microfinance remains a critical tool for people living in poverty, particularly women, to improve their quality of life and strengthen their resilience, even in the face of a crisis.

BRAC’s microfinance programme always intends to complement BRAC’s social development interventions to amplify the impact of BRAC’s work. A study in Uganda on 8,768 respondents reaffirmed that complementing microfinance with other sectoral interventions brings greater impact.

An experimental study in Liberia found that clients of BRAC’s Small Enterprise Loan product who received business-management skills and interpersonal skills trainings experienced an increase in attention to customers, which consequently enhanced the performance of the businesses, including higher average monthly revenue, less loss of customers, and a smaller likelihood of encountering business losses.

An experimental study in Uganda on 3000 women borrowers examined whether disbursing loans directly onto a digital account enables microfinance borrowers to grow their businesses. The study found that women who received their microfinance loan on the mobile money account had 11% higher levels of business capital and 15% higher business profits compared to a control group who received their loan as cash. Total household income and consumption were also higher.